As a highlight of the FIW workshop “Women in International Economics”, Secretary General Eval Landrichtinger (BMAW) and FIW Project Manager Univ.-Prof. Harald Oberhofer presented the FIW Award for Master Theses in International Economics to the two winners Nicole Sattler and Johanna Treiber.

Within the framework of the “Research Centre International Economics”, the “FIW Award for Women in Economic Research” is announced annually as a promotion for excellent young female scientists in the research area of International Economics.

This year’s prize was aimed at qualified female scientists who have written a diploma or master thesis at an Austrian university in the field of “International Economics” or Austrian citizens who have written their master thesis at a university abroad

The total amount of the sponsorship award is € 5,000; this year, the two winners will each receive € 2,500.

The winners are:

Nicole Sattler (BMF) for her master-thesis “The impact of the AfCFTA on the EU-Africa trade relation”

Johanna Treiber (Deutsche Bundesbank) for her master thesis “Labor Laws and FDI Productivity Spillovers – Analysis of the Labor Mobility Channel”.

It is important to study how other countries trade policies affects us. We often are only concerned with our trade policies. What others do matters! This is what we know from trade theory. Economic relationships with African economies will be crucial for tackling main challenges like climate change. Need for raw materials such a rare earths for green technologies. Technology transfer from EU to Africa crucial for development of global CO2-emmission.This is an excellent Master thesis, very well conducted and timely.

Harald Oberhofer on the justification of the FIW Award 2022 to Nicole Sattler.

This thesis applies state of the art econometric methods for studying an important question in the International Economics, namely on potentially positive effects of FDI for the host countries.The findings are relevant for understanding potential heterogeneity in positive FDI spillover effects for productivity also contributing to the policy debate on the role of host market institutions for the effects of FDI.This is important to our understanding of potential effects of technology transfer that might become relevant with respect to green technologies.

Harald Oberhofer on the justification of the FIW Award 2022 to Johanna Treiber.

After strong growth years, Austria’s foreign trade stagnates in 2023

After a dynamic development in 2022, the “Forschungsschwerpunkt Internationale Wirtschaft” (FIW) expects a low growth of Austrian exports and imports in 2023.

https://youtu.be/Aijw4S7luRU

FIW’s fourth annual report on the “Situation of Austria’s Foreign Trade” was presented together with Labor and Economics Minister Martin Kocher. The annual report is dedicated to the current international framework conditions for Austria’s foreign trade and trade developments in 2022. In addition, study authors Harald Oberhofer (WIFO, WU Vienna) and Robert Stehrer (wiiw) as well as study author Bettina Meinhart (WIFO) presented short- and medium-term forecasts for the expected future development of Austria’s foreign trade relations.

The year 2022 was dominated by the Russian attack on Ukraine and the subsequent energy price crisis. Households and companies were massively affected by the rise in energy costs. From the 2nd half of the year, the resulting supply shock and high inflation rates left their mark on the global economy. Austria’s dependence on Russian natural gas posed particular challenges for domestic households, companies and politicians. Austrian foreign trade held up relatively well under these difficult conditions, but suffered from the significant deterioration in terms of trade, i.e. a worsening of the relationship between export and import prices, in 2022. Prices for Austrian goods exports increased by 5.5 percentage points less than import prices. In pure volume terms, Austrian exports have developed more dynamically than imports: According to the forecast, total exports of goods and services rose by 8.8% in real terms in 2022, while imports increased by 5.1%.

In 2022, the negative terms-of-trade effect outweighed the quantity effect, so that in 2022 Austria’s trade balance deteriorated by €7.6 billion compared with 2021 and showed a deficit of €-20.5 billion. The more positive development of the services balance, which was driven by a massive increase in travel exports (more trips to Austria by foreign tourists), was able to offset the trade deficit last year. In 2022, the current account balance will be in positive territory at € 200 million.

For 2023, the “Research Centre International Economics” (FIW) forecasts growth in total exports of 0.3%. Imports are expected to rise by 0.9% this year. Mainly due to rising import prices – caused by the energy crisis – Austria could show a negative current account balance in 2023 for the first time since 2001. According to the forecast, the deficit will amount to € -1.8 billion (0.4% of GDP).

In 2023, the deterioration in terms of trade based on the study forecast continues with a decline of 1%. Exports of goods are expected to increase by 0.1%, with services exports recording growth of 1.2%. Total imports will grow by 0.9%. The difference between exports and imports results from higher services import growth of 3.3%. The trade balance could deteriorate to -€23.3 billion due to the further negative terms-of-trade effect. This deficit will no longer be fully compensated by the services balance surpluses. In 2023, the Austrian current account will show a negative balance with a deficit of €-1.8 billion (0.4% of GDP). According to the forecast, the current account should return to a small surplus in 2024.

One year ago, the world’s largest trade agreement, the RCEP agreement, was concluded. The trade of the EU and Austria with this region developed very dynamically in the last 20 years, with China playing the main role.

The RCEP Agreement

It has been exactly a year since another chapter of history in international trade was written and the largest trade block globally was formed. This resulted from the Regional Comprehensive Economic Partnership (RCEP) agreement implemented in January 2022, after ten years of negotiations. The RCEP gathered China, Japan, South Korea, New Zealand, Australia, and ASEAN countries into a unified trade block. This agreement assures the gradual elimination of tariffs between the RCEP members until 2040 and almost full commodity trade openness (90%). Great trade and growth implications globally are expected due to the size of this region. To demonstrate, RCEP countries together have approximately 70% higher GDP and over four times larger population than the EU. Thus, what we will likely witness in the next twenty years is a change in the gravity of the trade towards Asia-Pacific and away from the West (Quah, 2011; UNCTAD, 2021).

Strong momentum towards Asia even before the agreement …

Obviously, the dynamics whereby RCEP impacts the future of trade will mostly depend on China, RCEP’s dominant trade member. China alone takes up over half of the RCEP population and production. In addition, its role in international trade grew exponentially after its entry into World Trade Organization in 2001. Twenty years after its entry into WTO, EU trade with the RCEP members increased significantly: imports as a share of the total increased by 4.5p.p and export by 3.1p.p (see Figure 1, left). This trade boom with RCEP mostly attributes to China and at the expense of some other members like Japan whose export to the EU (as a share of the total) decreased from 2.8% to 1.2% over the corresponding period. The same narrative applies to Austria (Figures 1, right), although the RCEP 2020-2001 increase in trade share is smaller than for the EU as a whole.

… especially for high-tech products

However, the share of EU total imports from RCEP increased much more for high-tech goods (see Figure 2): from roughly 15% in 2001 to 24% in 2020. For Austria, the increase is even higher – a jump of 14p.p in the 20-year-period (Figure 2, right). Nowadays, almost 43% of total EU imports of computer, electronic and optical products, 26% of computer, electronic and optical products, and about 20% of machinery and equipment are sourced from the RCEP bloc. The export with the RCEP members also increased, although it represents lower shares of total EU and Austrian exports (see Figure 3).

This makes this sector particularly dependent and thus vulnerable given the further shift toward Asia and the potential changes in trade patterns resulting from the RCEP agreement. With this comes greater economic implications too, as the high-tech sector relies much more on R&D and innovation than traditional manufacturing. As such, high-tech sectors are an important catalyst of technological growth (Hornbeck and Moretti, 2018), especially in the times of digital and green transition. The obvious sign of risks already exists in relation to the recent semiconductor shortage, which put the production of many EU factories at a halt.

However, stagnation of trade relations in the last year

Even though only one year after the agreement implementation elapsed, we can witness a smaller decline or a stagnation of EU-RCEP trade (see Figure 1 and 2). EU export to the RCEP declined by about 1p.p, while Austrian high-tech imports from RCEP decreased by about 3p.p, the largest decline in high-tech trade with the new trade block in last 20 years. Not surprisingly, this shift is mostly driven by China alone (annual decline of 3.5p.p). This annual decline could be only a tip of the iceberg.

It is difficult to distinguish what drives this decline in the EU-RCEP trade as there are many factors at play. After the COVID-19 pandemic, new trends are on the trade horizon (i.e. nearshoring, reshoring, friend shoring) all marking the start of shorter supply chains, away from globalization. In line with this is RCEP trade bloc that is expected to contribute to the formation of the supply chain across the Asian-Pacific. On the other hand, the ‘EU’s Open Strategic Autonomy by 2040’ assumes a higher economic relationship between the EU and its neighborhood as well as its further trade positioning with respect to China. Besides this, the European Chip Act enacted in December 2022 aims to strengthen the resilience of the high-tech supply chains – precisely the EU semiconductor products for which the demand will double by 2030 according to the European Commission. All these trends should strengthen trade between geographically close countries at the expense of more distant countries. Hence, it is very reasonable to speculate that the next twenty years may bring lower trade with the RCEP due to trade distortion effects (see e.g. Stehrer and Vujanovic, 2022) resulting from the agreement, as well as further trade decoupling.

References

Hornbeck, R., & Moretti, E. (2018). Who benefits from productivity growth? Direct and indirect effects of local TFP growth on wages, rents, and inequality (No. w24661). National Bureau of Economic Research.

Quah, D. (2011). The global economy’s shifting centre of gravity. Global Policy, 2(1), 3-9.

Stehrer, R., & Vujanovic, N. (2022). The Regional Comprehensive Economic Partnership (RCEP) agreement: Economic implications for the EU27 and Austria (No. 054). FIW.

UNCTAD (2021), A new centre of gravity: The Regional Comprehensive Economic Partnership and its trade effects.

Nina Vujanović is an economist at wiiw, researching topics on international trade, foreign direct investment, and the Balkans. She previously worked as an advisor to the Vice Governor at the Central bank of Montenegro, as a consultant at UNCTAD (Division on Investment and Enterprise) and a research fellow at the WTO (Economic Research and Statistic Division). She published papers in the area of foreign direct investment, productivity, innovation as well as credit risk. She holds a PhD in International Economics from Staffordshire University and Msc in Economic Policy from University College London.

The interactive graphics were created by Alireza Sabouniha. He is a research assistant at wiiw and a master’s student in Economics at the WU (Vienna University of Economics and Business).

Since the start of 2022 the euro depreciated by some 15%, beginning the year at 1.14 USD per EUR and declining below parity towards 0.97 recently. One major factor causing this decline can be viewed as truly exogenous: the war in Ukraine was unexpected and resulted in several rounds of sanctions imposed on Russia, with sizeable negative repercussions on the EU’s export volumes and impairments for active foreign direct investment (FDI) of EU-firms in Russia. The EU received a second blow through rising energy prices. Many member countries showed a high dependence on Russian gas and oil, and the Russian government deliberately used its position to generate uncertainty in spot as well as futures gas markets leading to severe risk premiums after sanctions and countervailing measures by Russia were going back and forth. Due to its high dependence on Russian energy, the euro area suffered a set-back as a business location, making the euro area less attractive for passive FDI, destroying potential output, and finally leading to a depreciation of the euro vis-a-vis areas less exposed to Russia as a trade partner.

There is a second endogenous source for the devaluation of the euro, resulting from the build-up of inflationary pressure throughout the world economy, except Japan. The US-Federal Reserve Bank (Fed) was first confronted with rising inflation rates since in April 2021 (+4.2% YoY) while inflation in the euro area at that time still remained below target (+1.6% YoY). Both monetary authorities interpreted higher inflation rates as energy driven and transitory but by December 2021 the Fed changed its opinion and corrected its forward guidance from accommodative to restrictive. The Fed first announced to unwind its asset purchase program and started to increase the target rate by March 2022, while the ECB waited until the end of July 2022 to follow suit. By the end of September 2022 the target range for the US-interest rate reached 3% to 3.25% and the euro area‘s main refinancing rate was at 1.25%, creating an interest rate differential of almost 2 percentage points.

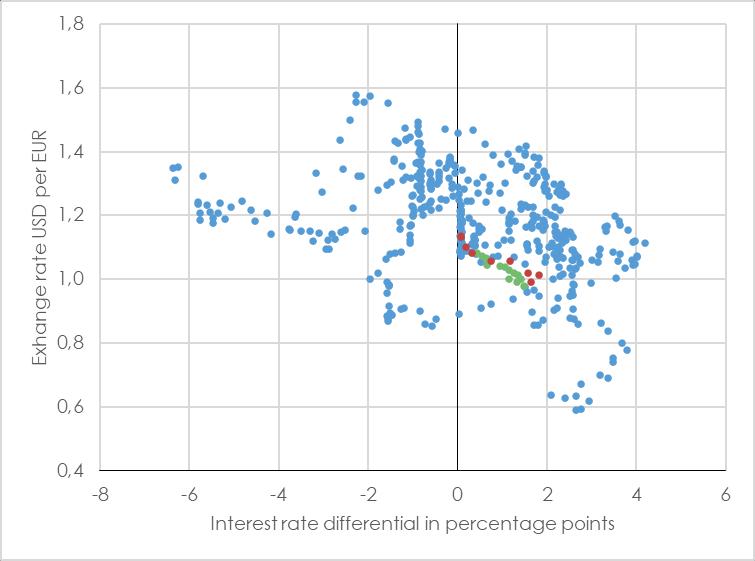

Deviations between US and European short term interest rates were a regular feature in the past. Figure 1 shows the interest rate differential between the US-target rate and the corresponding European equivalent from 1985 through 2022. A positive value on the horizontal axis implies that US-rates were above the main refinancing rate in the euro area. The vertical axis shows the exchange rate measured in USD per EUR. The slight negative slope of this cloud indicates that relatively high target rates in the US go along with a strong US-dollar, while a relatively high refinancing rate in the euro area typically involves a strong euro. The red dots in Figure 1 show the development from January to September 2022; the movement towards the lower right hand corner reflects the more aggressive policy stance in the USA together with the appreciation of the US-dollar.

Figure 1 – Relatively higher domestic interest rates support the home currency

Starting from this situation, what can we expect for the rest of 2022 and the following year? The WIFO forecast (Glocker – Ederer, 2022) expects a further tightening of monetary policy in both areas with the ECB acting more decisively such that the interest rate differential will be reduced to around 0.5 percentage points at the end of 2023. Accordingly, the euro will appreciate slightly (green dots in Figure 1), resulting in annual averages of 1.05 (2022) and 1.04 (2023) USD per euro with a trough in fall 2022. This development can be interpreted using the uncovered interest rate parity condition: after the US-monetary tightening, the USD must jump to a lower value (appreciation) in order to keep the interest parity condition valid, thus providing room for a consecutive depreciation which balances higher US-interest rates (Dornbusch, 1976). This adjustment mechanism does not hold empirically, however (Engel, 2014). A time-variable degree of asset market segmentation (Alvarez et al., 2009) or a liquidity premium on the deposit earning higher interest (Engel, 2016) provide alternative explanations.

Does the USD-EUR exchange rate actually jump around announcements dates of monetary policy actions? Figure 2 offers some insight. The lines in Figure 2 depict the exchange rate during the 10 business days before and after a monetary policy meeting, on which either the Fed (green) or the ECB (blue) announced a change in their target rate. To facilitate comparison, I norm the exchange rate for all episodes to unity at the day of the monetary policy announcement, thus a value of 1.02 indicates that the exchange rate was 2% above the level prevailing at the announcement date. The period runs from 16.3.2022, when the Fed published the first rate-hike through 21.9.2022, when the Fed increased the target range to 3% to 3.25%. Because both central banks explicitly use forward guidance, their moves appear to be somewhat expected. While the ECB does not seem able to move markets, the Fed announcements effectively make the dollar stronger, either at the date of the publication or even five to ten days ahead. Whether the ECB policy decision on 27.10.2022 includes some surprise element for the participants on the foreign exchange market, can be tracked in real time in Figure 2 over the next ten business days following the announcement date.

Finally, will there be consequences from the euro’s depreciation on the real economy? Probably price effects will dominate over the forecast horizon. A weaker euro implies higher import prices on intermediates, energy, consumer products, and tourism services in a period already plagued by inflationary strain. Such an environment makes it easier to pass-through higher import prices on to euro area customers. Positive wealth effects related to foreign USD-denominated portfolio investments by Europeans, however, will not compensate the price losses on international asset markets during 2022. Consequently, the potential positive effect on euro area consumption will remain limited. A cheaper euro will boost euro area exports, but at the same time weak foreign demand is likely to be the dominating force affecting international trade flows.

is Senior Economist at WIFO and has been working in the Research Group “Macroeconomics and European Economic Policy” since 1994. From 1999 to 2002 he was editor-in-chief of WIFO-Monatsberichte (WIFO Monthly Reports). He is an expert in the Austrian Fiscal Council, lecturer at the University of Vienna and head of the Working Group on Economic Statistics and National Accounts of the Austrian Statistical Society. He works on issues of risk diversification, funded pensions, the European Monetary Union and econometric applications in the field of macroeconomics.

The international economic environment has deteriorated significantly since the beginning of 2022, mainly due to the knock-on effects of the Russia-Ukraine conflict, and the outlook for the global economy and global trade has clouded considerably. The energy price shock and the massive price hike, as well as uncertainty about the availability of gas, are causing dislocations above all in material goods production and exacerbating supply-side shortages due to supply bottlenecks and the aftermath of the COVID 19 pandemic. Consumer confidence and corporate production expectations are falling worldwide, most sharply in the euro zone.

Domestic manufacturing and, in particular, exports proved to be very robust in the first half of 2022 in the face of the negative influences of massive increases in raw material and energy prices, labor shortages, supply bottlenecks and high uncertainty. Austrian merchandise exports expanded strongly in the first half of 2022, with extremely dynamic growth in Q1 2022, which – despite the onset of the Russia-Ukraine crisis in March 2022 – continued only slightly weaker in Q2 2022. The growth of exports of goods reached 19.2% at current prices (nominal) and 14.1% at constant prices (real) by June 2022. The widening gap between the nominal and real trends reflects rising export prices. Austria’s goods export performance was hardly outperformed by any other EU country. Germany, France and Italy recorded significantly lower growth, but goods exports of many smaller European comparator countries, such as Sweden, Finland or the Netherlands, also grew more slowly than in Austria.

Industrial intermediate goods (“processed goods”) have so far made one of the highest contributions to growth in total merchandise exports. This was a consequence of still stable industrial production through increased production in stock with key trading partner countries in order to escape threatened shortfalls in energy supplies and further price increases. The equally high contribution to growth made by Austrian machinery exports was due in particular to strong demand from the USA. The high order backlog in the German capital goods industry also contributed to growth in Austria’s machinery exports. The contribution from energy and raw material exports was mainly price-driven rather than due to an expansion in export volumes. The otherwise important Austrian automotive and automotive supply industry made hardly any contribution to export growth. This is closely related to the crisis in the German automotive industry.

Leading indicators, which remained at a high level until the end of Q2 2022, now also point to a sharp slowdown in export momentum in Austria in the second half of 2022. In the WIFO Business Survey, exporters continue to assess order books from abroad as predominantly positive, but the share of positive reports has declined significantly since June 2022. Export expectations have been significantly scaled back for the first time since the COVID-19 crisis, and negative expectations for export business predominate. As a result, the outlook for new export orders for the remainder of the year is much more subdued. In Q3 2022, export growth should still be fed by the high order backlogs of previous months and diminishing material bottlenecks in domestic production. In the further course of the year, the negative consequences of the Russia-Ukraine crisis are likely to have an increasing impact on Austrian exports of goods. Austria’s strong ties with the CEECs and Germany, which are particularly affected by the current crisis, will contribute to this, as will the expected decline in production in Austria’s manufacturing sector due to high energy prices – especially natural gas prices. This effect is amplified by the loss of international competitiveness, especially in non-European exports – currently, European and Austrian industry faces gas prices about seven times higher than those in the U.S., for example, and competitive advantages for exporters due to the devaluation of the euro hardly outweigh this. However, the direct negative effect of energy prices on manufacturing in Austria is likely to be somewhat weaker than in Germany, especially since the natural gas intensity of Austrian industry is somewhat lower.

The forecast assumes that there will be no official business closures due to the COVID 19 pandemic in Austria or in key trading partners that would affect the export industry until 2023. It is also assumed that the Russia-Ukraine war will continue and that the sanctions against Russia will remain in place. It is not assumed that Russia will completely halt natural gas supplies to Europe, but uncertainties, especially regarding price developments, are assumed to remain and thus the level of natural gas prices will remain high. In this environment, some of Austria’s main trading partners are facing a sharp economic slowdown, which will lead to recession in 2023 in Germany, Italy and CEEC. The revisions in the international economic outlook since the beginning of the year have been enormous, shaping the forecast picture of all major international organizations (European Commission, OECD, IMF, World Bank) and reflecting the increasing distortions of the Russia-Ukraine conflict and the strikingly higher world market prices of energy and raw materials. As a result of the cooling of the global economy in 2023, the problem of bottlenecks in supply chains should subside. The situation is also expected to ease for freight rates in international transport and for the prices of crude oil and industrial raw materials.

Under these changed conditions, Austrian export momentum will decline sharply, especially at the end of 2022, but supported by the extraordinarily good performance in the first half of 2022, will lead to annual growth in goods exports of around 8%, almost matching the previous year’s growth (2021: +9.3%). At 10.0%, import prices will rise much faster than Austrian export prices (+5.9%) in 2022. The high world market prices for raw materials, energy and intermediate goods thus cause a strongly negative terms-of-trade shock, which is further amplified by the depreciation of the euro. As a result, the Austrian trade balance will be burdened this year with a negative price effect of around € 8 billion. Positive volume effects due to a smaller increase in import volumes than in export volumes will dampen this negative effect, so that the trade balance is expected to deteriorate by a total of €4.3 billion in 2022 to a deficit of approx. 17 billion in 2022.

Im Jahr 2023 erreicht das österreichische Marktwachstum auf Basis der schwachen internationalen Importprognosen für die

In 2023, Austrian market growth will only reach around 0.4% based on weak international import forecasts for its trading partners. Above all, the gloomy economic outlook for Austria’s most important export markets in the euro area and the increasing deterioration in international competitiveness make it increasingly difficult to maintain market shares, especially in energy-intensive and important parts of the Austrian export industry (chemicals, steel, paper). Exports of goods in 2023 are stagnating, as are imports. The terms of trade, i.e. the ratio of export to import prices, will continue to deteriorate in 2023, to a much lesser extent than this year, but the negative price effects will nevertheless remain the main reason for the further increase in the trade deficit in 2023 by €2.6 billion to €19.7 billion.

is Senior Economist in the research area “Industrial Economics, Innovation and International Competition” and has been working at the Austrian Institute of Economic Research (WIFO) since 1992. From 2013 to 2016, she was Deputy Director of WIFO. She studied economics at the University of Vienna and received her PhD from the University of Innsbruck. Stays abroad at renowned universities in the USA (University of California, Los Angeles, and Stanford University) have accompanied her career since then. Her research focuses on the empirical analysis of international trade issues, including foreign direct investment. The preparation of the foreign trade forecast is one of her regular activities at WIFO.