The African Continental Free Trade Area (AfCFTA) is an ambitious initiative, full of promise for Africa and beyond. It comes at a time when the continent faces many development challenges. Africa hosts the largest group of developing countries in the world, of which 33 are least developed countries, and 16 are landlocked developing countries.

Introduction

With the adoption of the Agreement Establishing the African Continental Free Trade Area (AfCFTA) in May 2018, a new impetus has been given to Africa’s regional integration. The AfCFTA promises to connect 1.4 billion people across 54 of the 55 African countries (Eritrea is not participating), spanning of a market with a combined GPD of 3.4 trillion USD. It envisages the free movement of goods, services and people, and provides for continental rules on competition, investment, intellectual property, digital trade, and women and youth.

When looking at Africa’s recent trade performance, there was a positive post-pandemic rebound. Trade grew from $589 billion in 2021 to $689 billion in 2022. This 2-digit growth was above what was witnessed globally and in other regions. Nonetheless, the narrative of the continent’s poor participation in global trade has not changed. Africa’s share of world trade has hovered around 3% over the last decade, as shown in Figure 1. Though stable, this trade is overshadowed by the shares of other regions, for example Asia trading as much as 40% and Europe 37% of the global total.

Africa’s share in global trade hardly does justice to the continent. Africa hosts 25 per cent of global population, representing a consumer market which had an estimated worth of $1.4 trillion in 2015, and is projected to grow to $2.5 trillion by 2030. In this context, the AfCFTA forms part of the African Union’s Agenda 2063, which is the blueprint of Africa’s future vision. The AfCFTA is therefore seen as an opportunity for Africa to overcome major development challenges and integrate better through trade, both regionally and globally.

State of Play of the AfCFTA Negotiations

Since the historic entry into force of the Agreement which brought the AfCFTA to live in 2019, there has been important progress. A total of 47 of the 54 States Parties have ratified the agreement so far.

For trade in goods, an ambitious target has been set to achieve tariff liberalization for 97% of trade. State Parties, either in their individual capacity or as part of a Regional Economic Community (REC), have submitted tariff offers detailing goods subject to duty free trade, and also listing goods that are sensitive or excluded, representing the remaining 3% of trade.

For trade in services, negotiations have advanced in 5 priority sectors, namely business, communication, financial, tourism and transport services. Services schedules detailing the level of national treatment and market access afforded in these sectors have been submitted. In future liberalization rounds, other sectors will be negotiated, though some countries have already made offers in non-priority sectors such as health, education and recreational services.

Both for goods and services, the submitted schedules of commitments have and are undergoing technical verification processes to ensure they are compliant with what was agreed. To facilitate commercially meaningful trade in goods and services under the AfCFTA, there are also Guided Trade Initiatives in place for countries in need of support.

For the so-called AfCFTA phase II of negotiations, 3 protocols providing common rules on intellectual property, investment and competition, respectively, were adopted in February 2023. State Parties are now negotiating two additional protocols, on women and youth, and on digital trade, respectively. These are considered critical to unlock the full benefits of the AfCFTA, since women and youth are the backbone of the private sector and digital trade is a very dynamic sector, growing at a rate of 40% annually, and expected to exceed US$ 300 billion by 2025.

Accompanying the AfCFTA, the African Union members have also signed protocols supporting the free movement of persons and a single African air transport market, which are deemed to facilitate the mobility of people on the continent and free the commercial air transport market from various impediments, once they enter into force.

Expected Gains and Impacts of the AfCFTA

Historically, the composition of African trade has been characterized by trade of primary commodities with little value added. Though there has been some diversification in the destination of trade, increasingly with Asia and also with the continent itself, trade with Africa’s traditional partner Europe is still very dominant. As shown in Figure 2, on average, between 2016 and 2022, the EU led as Africa’s first trade destination, representing more than a quarter of the continent’s trade with the world (28.6% of its exports and 26.9% of its import shares, respectively). Of this trade, African exports and imports to and from Austria registered a 0.3% share of the global total on average.

The second place for Africa’s trade destination was tightly wrung between the continent itself and China. Intra-African exports represented 15.5% of Africa’s global trade share, closely followed by China (14.9%) and India (6.8%). African imports from China represented 17.8% of its global total, compared to 14%, 9.1% and 5% from Africa, the Americas and India, respectively. Trade with the rest of the world on average comprised almost a third of total African exports at 31.6%, and just over a fourth of total African imports at 26% for 2016-2022.

When taking a closer look at trade with Africa’s main trading partner, there are notable differences in the composition of the continent’ import and export patterns. As shown in Figure 3 below, African exports to the EU are primarily be characterized as a trade in extractive commodities, namely fuels (46%), followed by manufactures (28%) and food (14%), where there is generally little value addition from the continent. In comparison, when considering African imports from the EU, over two thirds are manufactures (67%), dwarfing processed food and fuels, each of the latter registering a 13% share. In contrast, intra-African trade paints a different picture. Within the continent, there appears to be more trade sophistication, with manufactures (45%) leading, followed by fuel (21%) and food items (20%).

With the AfCFTA, these trade patterns are expected to change. It is estimated that by 2045, intra-African trade will be 34% higher than without the AfCFTA. Trade in sectors such as agri-food, services and industries will increase by 49.1%, 37.9% and 35.7%, respectively. The expected increase in energy and mining will be lower, at 19.4%. With the AfCFTA, the value of intra-African trade is expected to increase with 577% by 2045 (as compared to a 405% increased in a scenario without the AfCFTA). This would translate into a net gain of intra-African trade creation estimated at USD 195 billion and the share of intra-African trade would expand from 15% today to over 26% by 2045.

Currently, the demand for trucks to transport bulk cargo in 2019 was registered at 698,000. Without the AfCFTA and infrastructure development as initially planned, this demand would only grow to 1.3 million, as compared to a full AfCFTA and infrastructure development scenario in 2045 where the demand for trucks for bulk cargo would increase to 1,9 million by 2030. Intra-African trade in transport services has the potential to increase by nearly 50%, whilst in absolute terms, over 25% of intra-African trade gains in services would go to transport alone; and nearly 40% of the increase in Africa’s services production will be in transport. This is encouraging when considering transport costs in Africa, which range from 15 to 20% of import costs, representing double and even threefold of the costs developed countries bare.

Trade and Investment Opportunities in Africa

Given the estimated gains and dynamic impacts of the AfCFTA, there are sizeable opportunities through Africa’s trade integration. The expected increase in market size will spur market efficiency, making Africa a more attractive destination of foreign investment and trade.

There is scope for deeper and services-based industrialization from within the AfCFTA as shown by the estimates for 2045. This trade is also expected to increasingly include intermediary goods for further processing within the continent, bolstering regional value chains.

Unlike world FDI which targets the natural resources sector, intra-African investment gravitates more towards services, particularly insurance, retail banking and telecommunications. The AfCFTA is thus an important vehicle to promote intra-African trade and investment, especially in the more dynamic sectors. For example, because of the new trade demand from the AfCFTA the increased need for trucks, rolling stock, aircrafts and ships translates into an investment opportunity of USD 411 billion. In sum, the AfCFTA opens opportunities for (both domestic and foreign) companies already operating on the continent, or for those thinking to establish a production base to source the African market.

Existing Challenges and Concerns of the AfCFTA

Though the AfCFTA is at its early stages, there are some important challenges and concerns. These range from multiple and overlapping REC memberships (see Table 1), to trade adjustment costs, the coexistence with other trade agreements and previous commitments and the capacity of the countries to domesticate the various protocols into national laws, policies and legislation in a timely fashion.

Among these, a major question is how the AfCFTA is going to coexist with other agreements and obligations which are already in place or being negotiated with other regions, such as the EU and China. With the EU, some countries have economic partnership agreements in place (see Table 1). The AfCFTA agreement will require countries to revisit such agreements considering the newly acquired obligations.

The AfCFTA is anticipated to contribute to reducing the current trade dependency on primary commodities of Africa on its external partners, including the EU and China, particularly in terms of industrial imports which could ultimately contribute to closing trade deficits of African countries with external partners. This is an opportunity for a shift towards more value added and intermediary trade patterns, from which Africa and its trade partners from beyond the continent stand to gain.

The Way Forward

The AfCFTA brings unprecedented opportunities for Africa’s transformation, competitiveness, and development. Though aspects of the AfCFTA negotiations are still evolving, it is important to monitor and support the implementation process of the agreement.

Effective implementation of the AfCFTA, will require the joining of efforts and various partnerships across global and regional spheres, which could help Africa and its business partners capitalize on the expected benefits and opportunities this megaregional has to offer.

Author:

Laura Páez is currently guest researcher at the Vienna Institute for International Economic Studies (wiiw). She is an international development practitioner with more than twenty years of professional experience. She is currently appointed to the United Nations Economic Commission for Africa (ECA), where she heads the Market Institutions Section. Previously she headed the Investment Policy Section at ECA. Her current work focuses on generating knowledge on the regulatory and policy dimensions across investment, competition, intellectual property, services and digitalization in Africa, geared to support regional integration processes such as the African Continental Free Trade Area.

Prior to her current appointment at ECA, Laura Páez worked at the United Nations Conference for Trade and Development in Geneva on issues pertaining to Africa’s economic development in the context of the continental’s trade and development agenda.

The interactive graphics were created by Alireza Sabouniha. He is a research assistant at wiiw and recently completed his master’s degree in Economics at the WU (Vienna University of Economics and Business).

The huge rise in prices and sudden shock in energy costs from the previous year, along with a significant decrease in precautionary stocks, will negatively impact global industrial production and world trade in 2023. Additionally, Austria’s inflation gap with vital trading partners and the euro’s increase in value worsen its competitive pricing position. Nonetheless, Austrian exports of goods experienced a robust 3.9% growth (in real terms)) during the first half of 2023, thereby increasing market share in crucial markets. Export growth will slow down considerably in the latter half of this year. In 2023, goods exports are expected to grow by approximately 1.5% (in real terms) overall. There is a likelihood that exports will increase by 2.5% (in real terms) in 2024. By 2023, the trade deficit in goods for foreign trade will be reduced to half the amount of the previous year, at € -10.3 billion. This improvement is partly due to a decrease in energy prices, which has positively affected the terms of trade. Figure 1 presents a summary of the primary outcomes of the foreign trade forecast.

Global economic output loses momentum and dampens growth in Austrian export markets

Global economic development has recently lost considerable momentum (see Figure 1.1). It is accompanied by a weakness in global industrial production, which is also having an impact on global trade in goods. Germany is particularly affected by this. Austria’s most important trading partner is expected to experience a recession in 2023 (-0.6%), while Germany’s economic output will recover slightly next year (+1.2%). The economy in Europe will also be burdened by high inflation and rising interest rates as a result of restrictive monetary policy. At the same time, demand in China declined significantly following the end of the lockdown in spring 2023. However, global industrial production and trade in goods are also falling, primarily because of the reduction in precautionary stocks that were built up in previous years due to the threat of supply shortages and energy supply shortfalls. However, the shift in the global consumption structure from increased consumption of goods to increased consumption of services – due to the coronavirus – is also having a dampening effect. The growth prospects will only improve again next year with the advanced reduction of increased inventories. In addition, most of the forecasts currently available indicate a further decline in inflation for 2024. The continuing restrictive monetary policy and weak economic development in China are likely to have a negative impact on the global economy in 2024. In the US, the economy has remained stable so far and has been supported primarily by private consumption. However, economic growth is also forecast to weaken in the US in 2024, primarily because the impetus from private consumption is fading.

Inflation differential to other countries and appreciation of the euro worsen the competitive price position

Under these international conditions, the Austrian export markets (the “Austrian market growth”) will shrink by 0.4% this year, mainly due to weak import demand from Germany and the Central and Eastern European countries and are expected to recover by +3.2% in 2024 (Figure 1.3). In addition, Austria’s inflation gap with important trading partners and the appreciation of the euro will lead to a deterioration in its competitive price position in the forecast period (Figure 1.3). In 2023, the price increase measured by the consumer price index is significantly higher than in comparable countries in the eurozone (Figure 2.1). This inflation differential is likely to shrink in 2024 but will continue to persist. In line with this picture, domestic industrial companies once again rate their competitive position as significantly worse compared to competitors in the EU, but especially compared to competitors outside the EU (Figure 2.4). Assessments of the competitive position have reached historic lows, particularly in the intermediate goods and consumer goods sectors, while the decline in the capital goods sector has been delayed and less severe. However, an effect on Austria’s exports and market shares cannot yet be seen in the data for the first half of 2023.

Robust development of goods exports and market share gains in the first half of 2023 despite adverse circumstances

The Austrian export industry proved to be robust in the first half of 2023 despite the negative influences and was even able to gain market share in important markets. It is less affected by the slump in demand for primary products in the wake of destocking and was able to maintain its competitiveness in specific niches. The development of Austrian producer prices abroad also suggests a moderate pass-through of domestic cost increases to Austrian export prices relative to trading partners, presumably at the expense of corporate profits. According to preliminary data from foreign trade statistics, growth in exports of goods reached 6.1% at current prices (nominal) and 3.9% at constant prices (real) in the first half of 2023 (Figure 3). Exports of capital goods (machinery and vehicles) proved to be the most important growth drivers. The (nominal) market share development in the first half of 2023 shows gains of 10.2% compared to the same period of the previous year, mainly thanks to strong exports of machinery to Germany and the USA. Measured in terms of exports in the eurozone, Austria’s market share rose by 3.4%1).

Pessimistic outlook for the second half of 2023, but moderate recovery in the coming year

However, company assessments in the WIFO Business Survey convey a pessimistic outlook for the second half of 2023 (Figures 4.1, 4.2). The assessment of export orders has deteriorated since the May survey. Export expectations were also downgraded significantly in the summer months and barely recovered in the last survey in October. The mood in the capital goods sectors has deteriorated, and thus in the very areas of the export industry that have driven export growth to date. This should slow down export momentum in the second half of 2023 and significantly diminish the export successes from the first half of the year. Growth in goods exports of around 1.5% (in real terms) is expected for 2023 as a whole (Figure 5.1). Given the assumption that the international economy will improve in 2024, a recovery can be expected over the course of the coming year. Exports of goods are likely to increase by 2.5% (in real terms) in 2024. However, the now delayed decline in demand for capital goods will extend into 2024 and leave Austrian export companies specializing in capital goods little room for further market share gains.

Imports of goods reflect the weakness of domestic industrial production and the reduction in precautionary stocks of energy and industrial raw materials that were built up in the previous year. In addition, the slump in the consumption of so-called consumer durables in particular is also noticeable2). This is also partly due to the normalization of the consumption structure following the COVID-19 crisis. Imports are expected to fall by almost 2% (in real terms) in 2023, while imports are likely to recover in 2024 with growth of 2.3% (in real terms) (Figure 5.1). The trade deficit in foreign trade in goods will improve significantly due to the weak import trend and, at € 10.3 billion, will be half of the previous year’s figure in 2023 (Figure 5.2). However, the improvement in the terms of trade, the ratio of export to import prices, is also essential for foreign trade. These had deteriorated drastically in 2022 as a result of commodity and energy taxes – particularly due to the higher proportion of energy in imports – and weighed heavily on Austria’s trade balance. However, the fall in energy prices (especially for natural gas) this year triggered a countermovement. he natural gas and crude oil became more expensive. According to the current forecast, the major price pressure from abroad via commodity prices will continue to ease, and the increase in producer prices for goods sold abroad by Austria and important trading partners in the EU has also continued to weaken. The terms of trade will therefore improve again in 2023 and 2024 (by +1.5% in 2023 and +0.5% in 2024), but less significantly than they deteriorated in 2022 (-5.0%) (Figure 5.3). Key imported commodities such as natural gas and crude oil will also remain more expensive in the medium term.

The forecast is based on the assumption that there will be no further escalation in Russia’s war of aggression against Ukraine, that sufficient natural gas stocks have been built up over the winter and that a complete halt in natural gas supplies from Russia to Europe can still be ruled out. Nonetheless, potential dangers persist, and deficits might lead to more expensive prices and fuel inflation. The recent Middle East conflict between Israel and Hamas also harbours additional uncertainty and geopolitical risk if the conflict spreads and further tensions in the Middle East jeopardise the production and transport of oil. However, if none of this happens, inflation may drop faster than predicted in the forecast, resulting in the possibility of raising the key interest rate, which would give a positive boost to the global economy.

Autorin:

Dr. Yvonne Wolfmayr is Senior Economist at WIFO and has been working in the Research Group “Industrial, Innovation and International Economics” since 1992. From 2013 to 2016 she was Deputy Director of WIFO. She studied Economics at the University of Vienna and the University of Innsbruck with a major in International Economics. Since then, she has spent time abroad at renowned universities in the USA (University of California, Los Angeles, and Stanford University). Her research focusses on the empirical analysis of international trade issues, including foreign direct investment The foreign trade forecast is one of her regular activities at WIFO.

The development of nominal market shares also reflects price and exchange rate changes. If the market share is calculated in comparison to countries in the same currency area, the exchange rate effect is eliminated in this comparison. ↩︎

Consumer durables include furniture, sports equipment, bicycles, refrigerators and washing machines, for example ↩︎

This FIW Spotlight focuses on the impact of sanctions on trade by the European Union (EU) and Austria with Russia. The imposition of sanctions has led to a significant drop in trade, with a 40% drop in EU exports to Russia and a 19% drop in Austrian exports. Remarkably, Russia bears the economic cost of these sanctions, as illustrated by a significant GDP loss of 7.9% on a permanent basis. This analysis shows the profound impact of sanctions on international trade relations as well as the economic losses of the sanctioned country, in this case Russia.

The invasion of Ukraine by Russia in February 2022 has led to a wave of outrage around the world and triggered a complex response of sanctions and counter-sanctions. These policies not only have a direct impact on the nations involved, but also send shockwaves through the global economy that reach far beyond the countries directly affected. At a time when the global economy is still struggling with the aftermath of the COVID-19 pandemic, understanding the economic costs of these sanctions is crucial.

At the beginning of the conflict, studies were published promptly that analysed the economic costs of possible sanctions and trade stops (Bachmann et al., 2022; Balma et al., 2022). At that time, however, it was not yet possible to measure the exact impact of these measures on trade. The authors could only make assumptions and create models. Seventeen months later, it is now possible to measure the changes in trade volumes and thus provide a precise analysis of the costs of these measures. First, the author takes a look at the impact of the sanctions on trade before examining the macroeconomic consequences in more detail in a hypothetical scenario.

Trade collapses

The sanctions taken have had a significant impact on trade with Russia. EU exports to Russia plummeted by over 60% when the first set of sanctions came into force in May 2022. Subsequently, exports have recovered somewhat. However, they were still 40% below the multi-year average in January 2023. These aggregate figures at the EU level do not give an indication of the differences in trade depression between member countries (see chart 1). Among the largest member countries, France’s and Germany’s exports to Russia fell the most. German exports in January were 59% below the long-term average, French exports 48% below. Austria’s trade with Russia was less affected. Austrian exports initially fell by 41% in May 2022. They then recovered and even reached a plus of 2% in July 2022. Nevertheless, the sanctions also have a negative impact on trade for Austria. In January 2023, exports were still 19% below the multi-year average. The different trade effects between the member states show that the countries trade very different goods with Russia. Each “basket of goods” contains different shares of sanctioned goods and services. For example, the Austrian export mix contains an above-average number of non-sanctioned goods groups, such as food and pharmaceutical products, which explains the small decline.

In order to calculate the economic impact of the sanctions, the different “baskets of goods” of the countries in trade with Russia must be taken into account. To do this, the author first calculates the sanction effect at the level of different product groups using the so-called “gravity equation” from the international trade literature (Head and Mayer, 2014). Subsequently, the author uses these sanction effects in a model of international trade (Felbermayr et al., 2023). This allows the author to explore the following “what if” scenario: What would the world look like if there were only the Russia sanctions, but all other economic influencing factors were held constant? Since all other influencing factors are excluded – for example, other crises or political measures in the past year – the “pure” effect of the sanctions can be examined.

Russia bears the brunt

The calculations show that Russia clearly bears the costs of the sanctions (see chart 2). Russian GDP falls by 7.9% in the long term due to the sanctions imposed by the West and Russian counter-sanctions. This means that the sanctions alone permanently lower the level of the Russian economy. In other words, without the sanctions, Russian society would be 7.9% “richer”. The effect remains even if the Russian economy were to grow again in real terms in the future.

In contrast, GDP in the EU decreases by only 0.21%. This corresponds to a sum of 33 billion euros. Of the large member states, Germany is the hardest hit. German GDP falls by 0.26%. This is mainly due to its dependence on energy imports from Russia. In Austria, GDP falls by 0.2% and is thus slightly below the EU average.

Austrian exports fall by 1.7%. Pharmaceutical products (-9.5%) and other transport equipment (-8.6%) are the most affected. Machinery and equipment (-4%) and electronic equipment (-2.2%) are other export-strong sectors that are negatively affected (see chart 3). However, some sectors also benefit from the sanctions. Not surprisingly, exports of petroleum (11.9%) increase significantly. Austria can take over part of the lost Russian exports here. The production of petroleum refers to the processing of crude oil. Austria does not produce oil, but processes more imported oil than before the sanctions, when petroleum was also imported directly from Russia to the EU. Other sectors that benefit from the sanctions are the production and casting of metals and the mining of metal ores, whose exports each increase by 1.6%.

The analysis of the Russia sanctions highlights the complex and far-reaching impact of policy measures on the global economy. While the sanctions hit Russia significantly, with a long-term GDP loss of 7.9%, the impact on the EU as a whole is smaller but still noticeable. The Austrian economy can absorb some of the West’s sanctioned trade flows with Russia. However, it is not enough to offset the economic costs for Austria.

Author:

Hendrik Mahlkow has been working an an economist in the WIFO Research Group “Industrial, Innovation and International Economics” since 2023. He is a quantitative trade economist who is mainly interested in environmental economics and geopolitics. Using large computational general equilibrium models, he calculates so-called counterfactual scenarios: “what-if” considerations that allow to evaluate planned policy measures ex ante, or to review already implemented measures ex post. He is pursuing a PhD in Quantitative Economics at the Christian-Albrechts-University of Kiel. Most recently, he spent a research semester at the University of California, Berkeley.

References:

Bachmann, Ruediger, David Baqaee, Christian Bayer, Moritz Kuhn, Andreas Löschel, Benjamin Moll, Andreas Peichl, Karen Pittel, and Moritz Schularick, “What if? The economic effects for Germany of a stop of energy imports from Russia,” Technical Report, ECONtribute Policy Brief 2022.

Balma, Lacina, Tobias Heidland, Sebastian Jävervall, Hendrik Mahlkow, Adamon N Mukasa, and Andinet Woldemichael, “Long-run impacts of the conflict in Ukraine on food security in Africa,” Technical Report, Kiel Policy Brief 2022.

Felbermayr, Gabriel, Hendrik Mahlkow, and Alexander Sandkamp, “Cutting through the value chain: The long-run effects of decoupling the East from the West,” Empirica, 2023, 50 (1), 75–108.

Head, Keith and Thierry Mayer, “Gravity equations: Workhorse, toolkit, and cookbook,” in “Handbook of international economics,” Vol. 4, Elsevier, 2014, pp. 131–195.

The Russian invasion of Ukraine also put the Caucasia region into the spotlight of the European and Austrian public.

This Spotlight looks at the region’s trade ties with the EU and Austria, their significance for the region and the varying depth of the region’s relations with the EU. Georgia is the country with the currently deepest economic integration with the EU – along with Moldova and Ukraine – through a Deep and Comprehensive Free Trade Agreement (DCFTAs) followed by Armenia’s Comprehensive and Enhanced Partnership Agreement (CEPA), while Azerbaijan’s trade relations with the EU are still governed by a Partnership and Cooperation Agreement (PCA).

Selected key facts on Caucasia

The Caucasus region comprises of Armenia, Azerbaijan, and Georgia. Both in terms of population size and territory the region is comparable to the six West Balkan (WB6) states (Albania, Bosnia and Hercegovina, Kosovo, Montenegro, North Macedonia, and Serbia). The three Caucasus states have a population of 16.6 million and cover 186 thousand km², while the WB6 have 17.7 million inhabitants at an area of 204.5 thousand km² (WDI, Eurostat). To contextualise, Azerbaijan is slightly bigger than Serbia, Armenia is comparable in size to Albania and Georgia is slightly bigger than Bosnia and Hercegovina and Montenegro. In terms of GDP per capita (in PPPs), Georgia’s GDP is comparable to the level of Bosnia and Hercegovina, Armenia’s to Albania’s, Azerbaijan has the lowest GDP per capita in Caucasia (Figure A).

The domestic political situation of the three countries is heterogeneous. Among the three countries Azerbaijan ranks by far worst in corruption and press freedom. To illustrate, Azerbaijan ranks 157th corruption perception and 151st in press freedom. Armenia was ranked 63rd in the corruption perception index, while Georgia was ranked 41st. In the press freedom index Armenia ranked 49th lies ahead of Georgia, which was ranked 77th. By way of comparison, Montenegro ranks 65th in corruption perception while in press freedom Romania ranks 53rd and Hungary 72nd.

Trade ties

The overall share of goods exports of regional GDP was 38 % in 2022 while imports stood at 29 %. The regions exports are dominated by Azerbaijan which accounted for 80 % of the region’s total share, followed by Georgia (11 %) and Armenia (9 %) in 2022. This can be attributed to Azerbaijan’s well endowment with fossil fuels and the resulting exports thereof. The share of imports is more balanced, 41 % of which were imported by Azerbaijan, 35 % by Armenia and 24 % by Georgia.

The most important trading partners for the region are the EU, Russia, and Turkey (Figure B). These top three partners accounted for 74 % of the region’s exports and 54 % of its imports as share of total in 2022. As export partner the EU clearly takes the lead, 57 % of all exports went to the EU in 2022. The significant increase in exports to the EU in 2021 and 2022 can be attributed to surging energy prices and the high share of fossil fuels in exports to the EU. In 2022, Russia overtook the EU as leading import partner though by a narrow margin of one percentage point. Overall, the war in Ukraine has not materialised in large shifts in third country trade patterns until now. Compared to the significance of the region’s trade ties with the EU, its significance for the EU is of a much smaller nature. EU – Caucasia trade accounted for 1.1 % of the EU’s imports as share of extra-EU imports and 0.28 % of the EU’s exports in 2022. To compare, the WB6 accounted for 1.2 % of the EU’s imports and for 1.9 % of its exports.

Exports to the EU are clearly dominated by oil and gas, which accounted for 94 % of Caucasia’s exports to the EU in 2022, dwarfing the remaining sectors (Figure C). European exports to the region are more diversified, both in terms of sectors and destination countries, manufacturing being the most important sector. 41 % of EU exports alone are machinery and transport equipment.

Trade ties with Austria

For Austria Caucasia’s share in Austrian imports and exports (excluding intra-EU trade) is even smaller compared to the EU. Imports from Caucasia accounted for 0.08 % as share of non-EU imports and for only 0.003 % of its non-EU exports. Despite these rather small shares, this region has been a focal region for Austrian foreign policy. Austria has dedicated ambassadors for all three countries though the ambassador to Armenia is based in Vienna and the region is also a focal region for Austrian development policy. Two out of eight focal regions are in Caucasia (namely in Armenia and Georgia) where consequently the Austrian Development Agency (ADA) also maintains offices.

The main Austrian imports from Caucasia are mineral fuels, which are unsurprisingly dominated by Azerbaijan, while the key Austrian exports are machinery and transport equipment, manufactured goods and foods. Austria maintains a positive trade balance with the region. In 2022, it imported goods worth 62.6 million Euro compared to exports to the region amounting to 154.3 million Euro.

Energy Supplies

Caucasia is both an important transit route and source of oil and gas supplies for the EU. Azerbaijan’s gas is exported through the South Caucasus Pipeline via Georgia into Turkey from where it is also exported via the Trans Anatolian Pipeline (TANAP) to European markets. In light of Russia’s efforts to weaponize gas supplies, diversifying gas supplies has been a key goal of the European Commission.

Azerbaijan was the EU’s ninth biggest oil supplier in Q1 2023 (in Q1 2022 it was tenth), but fifth biggest gas supplier in Q1 2023 (Figure E). What figure E also illustrates, is the diversification away from Russian gas from almost 39 % of all extra-EU natural gas imports in Q1 2022 down to 17.4 % in Q1 2023. As part of this strategy the EU and Azerbaijan signed a new Memorandum of Understanding on a Strategic Partnership in the Field of Energy on July 18th, 2022.[1] Though a reasonable step to diversify gas supplies away from Russia, the increased cooperation with Azerbaijan (much like that with Qatar) has also earned the European Commission criticism for putting geopolitics over upholding European values, considering Azerbaijan’s track record with regards to human rights and fundamental freedoms.[2]

A conflict ridden region

Overall, the significance of the region for the EU and Austria is less of an economic than of a political nature. All three countries are involved in unresolved conflicts with one of its neighbours, namely the Nagorno Karabakh conflict between Armenia and Azerbaijan and the conflict of Georgia with Russia over South Ossetia and Abkhazia, regions effectively controlled by Russia.

The Nagorno Karabakh conflict was the most violent conflict which erupted in the wake of the immediate fall of the Soviet empire, resulting in two big wars in 1992 -1994 and 2020. In the first war Armenian forces had conquered the predominantly ethnically Armenia region of Nagorno Karabakh and surrounding territories which are internationally recognised as Azerbaijani, while in the second war Azerbaijan again reconquered the surrounding territories and approximately one third of Nagorno Karabakh.

One indirect consequence of the Ukraine war is the EU’s increased role as actress in conflict moderation, which gained considerable momentum in 2022. In Georgia the EU has been present with its EU Monitoring Mission (EUMM) (and theoretically also in Abkhazia and South Ossetia, theoretically as the EUMM has not gotten access to Georgian territory not under the control of Georgia’s government), while in the Nagorno Karabakh conflict it had been forced to remain on the sidelines only until recently. Azerbaijan’s military victory in 2020 and further flare-ups have put Armenia both under increasing domestic and external pressure. Russian inaptness or unwillingness to support Armenia has brought the EU to the table. In autumn 2022 a civilian EU monitoring mission to Armenia (EUMA) was set up and also several rounds of peace negotiations chaired by the EU have taken place since autumn 2022.

The varying depth of political relations with the EU reflects the differing ambitions of these three states towards European integration, with Georgia and its accession bid clearly taking the lead. Georgia has signed a DCFTAs (Deep and Comprehensive Free Trade Agreement) as part of its Association Agreement which have been in force since 2016. Armenia has upgraded its initial PCA (Partnership and Cooperation Agreement) to a CEPA (Comprehensive and Enhanced Partnership Agreement), which has been in force since 2021 while Azerbaijan’s trade relations with the EU are still governed by a PCA dating back to 1999. A similar pattern can also be observed with membership in the Energy Community an international organisation seated in Vienna “which brings together the European Union and its neighbours to create an integrated pan-European energy market.”[3] While Georgia is a contracting party like the WB6 states, Armenia has observer status and Azerbaijan is not associated at all. The war in Ukraine has changed the political dynamics. Ukraine and Moldova have been granted accession candidate status, while Georgia also applied though it is pending the green light from the European Commission given it makes progress in areas such as the judiciary system, fighting corruption and fighting organised crime. Above all the granting of candidate status is a significant policy shift, given that prior economic and political integration of the EU’s neighbours outside the Western Balkans has been characterised by applying enlargement methodology without the actual prospect of EU accession.

Conclusion

The EU is the key trading partner for the Caucasia region which also the Russian war against Ukraine has not changed. While European imports are dominated by fossil fuels, European exports are in particular manufactured goods. This is a pattern which also applies to Austrian trade with Caucasia, with key differences being that Austria maintains a positive trade balance with the region and the share of fossil fuels in its imports is lower. The significance of the EU’s role as key trading partner has not transformed into a deepening of political ties as the differing trade agreements (EU-Georgia DCFTA, EU-Armenia CEPA and EU-Azerbaijan PCA) and membership in the Energy Community shows, but the Russian war in Ukraine has. From a European perspective the region is particularly significant for (geo)political reasons, for its location in the EU’s south-eastern neighbourhood and gateway to Central Asia, and in the short to mid-term as supplier and transit route for energy.

Bernhard Moshammer is Economist at wiiw. His research focuses on European economic and political-economic issues. He has previously worked for the Austrian Federal Chancellery on EU affairs and on housing policies at the Austrian Chamber of Labour. He holds a degree in Economics from the Vienna University of Economics and Business and an M.A. in European Interdisciplinary Studies from the College of Europe, Natolin Campus in Warsaw, Poland.

The interactive graphics were created by Alireza Sabouniha. He is a research assistant at wiiw and a master’s student in Economics at the WU (Vienna University of Economics and Business).

The Turkish economy has been struggling in recent years, experiencing rapid depreciation of the lira and a surge in inflation. While this may appear to resemble the emerging market difficulties of the 1990s, and also partly reflects the inflationary pressures affecting all of Europe at the moment, the underlying mechanisms are distinct and mostly self-inflicted. The recent economic situation in Turkey, the 6th most important trade partner for the EU with 3.3%, serves as a stark reminder of the consequences of mishandling monetary policy.

The European Union continues to be Turkey’s largest export and import partner (Figure 1) despite a declining trend in the recent years. Between 2018 and 2022, Turkey’s export share to the EU decreased from 43.1% to 40.5%, while the import share dropped from 33.3% to 25.6%. Austria represents a smaller portion of Turkey’s overall trade: Turkey’s export share to Austria remained relatively stable at around 0.7% over the last years, the import share however dropped from 0.7% in 2018 to 0.5% in 2022.From the European perspective, Turkey is the 6th most important trading partner for the EU with 3.3%. Turkey’s share in Austrian trade is about 0.7% (incl. intra-EU trade).

Over the past decade, Turkey has faced a combination of challenges including unstable growth rates, significant currency devaluation, and surge in inflation (Figure 2). In recent years, the issues have worsened, partially due to external factors such as the COVID-19 pandemic and the war in Ukraine, leading to very imbalanced pattern of growth and a significant accumulation of potential risks within the economic system. Turkish unconventional monetary policy, characterized by low interest rates and heavy reliance on credit, has played a significant role in exacerbating these issues. With President Erdogan securing another term, concerns over the direction of the monetary policy are stronger than ever and raising alarms for the future stability of Turkey’s economy.

However, it is important to note that the economic landscape hasn’t always been this way. In fact, during the first 10 years of President Erdogan’s rule, both he and the AKP were widely regarded as capable, conservative, and careful in their approach to economic policy. Yet, from the mid-2010s, Turkey started grappling with significant challenges. Political risk increased, such as due to Gezi Park protests in 2013 and coup attempt in 2016. Partly in response to this, the government started to erode the capacity and independence of state institutions.

In an effort to counter the economic slowdown during that period, the government implemented measures such as substantial infrastructure investments and low interest rates to encourage domestic borrowing (Figure 3). The impression increased that the central bank was being forced to keep interest rates low. However, these measures resulted in significant trade deficits, increased reliance on external credit, rapid depreciation of the lira, and a loss of confidence in monetary policy driven by prolonged periods of negative interest rates and mounting inflationary pressures.

Turkish monetary policy experiment as a cure for slowing growth and increasing inflation

Central bank independency in Turkey has been on decline in recent years. President Erdogan’s actions indicate that he does not hesitate to dismiss central bankers and finance ministers if they do not comply with his wishes. Since 2020, three officials were dismissed from their positions without a clear explanation, sparking speculation that their refused to lower interest rates may have been the primary reason for the termination[1]. President Erdogan believes that higher interest rates are the cause of rising prices, not a cure for them. He argues that keeping interest rates low will encourage consumer spending, business investment, and job creation. He also claims that a weaker Turkish lira against the US dollar would make exports more affordable, leading to increased demand from foreign consumers.

There is some truth to his arguments. The weaker lira does seem to have helped export growth in the last couple of years. And cheap credit has certainly supported consumer spending. Yet these policies entail significant consequences. Turkey heavily relies on imports such as fuel, gas, medicine, fertilizer, and other raw materials. When the value of the lira declines, the cost of purchasing these goods increases. Additionally, President Erdogan’s unconventional monetary policy has raised concerns among foreign investors who were previously willing to lend substantial amounts of money to Turkish businesses. Furthermore, implementation of lira saving scheme “KKM”, a state-backed foreign exchange-protected deposit, is transferring the risk of exchange rate fluctuations to the public sector, giving a rise to substantial contingent liability, and posing a risk for domestic financial stability.

At the beginning of 2022, when central bankers in Europe and the United States started to adapt tighter monetary policies by raising interest rates to tackle inflation, Turkish Central Bank started lowering its interest rate. This unconventional strategy has led to sharp depreciation of the lira and ever-more elevated inflation rates, with the year-on-year inflation rate reaching a 24-year high of over 85% in October 2022. Many analysts believe that the actual inflation rate on the streets is even higher than the official figures suggest [2].

To counter the impacts of surging inflation, the Turkish government has implemented several measures. These include raising the minimum wage and public worker wages by 55% and 45%, respectively. Beside the introduction of KKM scheme, the government has also enforced strict regulations on foreign-currency transactions conducted by companies. However, the effectiveness of these measures appears to be limited. As of April 2023, Turkey’s annual inflation rate was 43.7%, showing a downward trend due to base effects, but still extremely high compared to peer countries.

Rising inflation rates in Turkey, along with an increase in import prices and production costs, create major difficulties for households and businesses alike. Low-income households struggle to afford basic necessities as prices skyrocket, while businesses find it challenging to plan and invest in new projects due to unpredictable returns and mounting costs. In Turkey, just like in any other country, inflation is influenced by factors related to both demand and costs. Therefore, raising interest rates alone would not address the issue. It is essential to also keep in mind cost factors such as higher energy prices. Yet it remains clear that as long as real interest rates are deeply negative, the lira will depreciate, imported inflation will surge, and the economy will suffer.

What does the future hold?

With President Erdogan securing another term in office, immediate changes to monetary policy following the elections are unlikely. However, considering President Erdogan’s history of policy changes, and the pressure of the weakening lira and high inflation on the economy, a change of course is possible. If the central bank does raise interest rates, this would not be the first time that it has abruptly changed course; something similar happened in 2018 and 2020. The timing of any reversal will depend on the economic consequences of the current policies. If the lira continues to decline, the state’s contingent liabilities, linked to KKM and other potential risks will escalate. Thus, it remains plausible that adjustments may be made.

Accurately assessing demand and cost factors remains crucial for effectively managing inflation and utilizing interest rate policy in Turkey. A change in the monetary stance to something more orthodox, targeting small positive real interest rates, would not solve all of Turkey’s economic problems but certainly improve macroeconomic stability and provide the basis for a more stable growth rate. However, even without this, the economy has shown itself remarkably resilient. If foreign funding continues to arrive to plug the large current account deficit, it is likely that the year 2023 will end with a growth rate of around 2.6% and an inflation rate ranging between 40-50%, gradually easing the pressure on the exchange rate throughout the year.

Meryem Gökten is Economist at the Vienna Institute for International Economic Studies (wiiw) and country expert for Turkey. Her research focuses on macroeconomic analysis, fiscal policy, and monetary policy. Prior to joining wiiw, she worked as a researcher in the Financial Markets and Institutions Unit at Centre for European Policy Studies (CEPS), and as a consultant in the Country and Financial Sector Analysis Division at the European Investment Bank (EIB). She holds a master’s degree in economics from University of Freiburg and bachelor’s degree in economics from University of Heidelberg.

Richard Grieveson is Deputy Director at wiiw and Research Associate at the Diplomatic Academy of Vienna. He specialises in the economies of Central, East and Southeast Europe, with a particular focus on Turkey and the Western Balkans. Previously he worked as a Director in the Emerging Europe Sovereigns team at Fitch Ratings and Regional Manager in the Europe team at the Economist Intelligence Unit. He holds degrees from the universities of Cambridge, Vienna and Birkbeck.

The interactive graphics were created by Alireza Sabouniha. He is a research assistant at wiiw and a master’s student in Economics at the WU (Vienna University of Economics and Business).

One year ago, the world’s largest trade agreement, the RCEP agreement, was concluded. The trade of the EU and Austria with this region developed very dynamically in the last 20 years, with China playing the main role.

The RCEP Agreement

It has been exactly a year since another chapter of history in international trade was written and the largest trade block globally was formed. This resulted from the Regional Comprehensive Economic Partnership (RCEP) agreement implemented in January 2022, after ten years of negotiations. The RCEP gathered China, Japan, South Korea, New Zealand, Australia, and ASEAN countries into a unified trade block. This agreement assures the gradual elimination of tariffs between the RCEP members until 2040 and almost full commodity trade openness (90%). Great trade and growth implications globally are expected due to the size of this region. To demonstrate, RCEP countries together have approximately 70% higher GDP and over four times larger population than the EU. Thus, what we will likely witness in the next twenty years is a change in the gravity of the trade towards Asia-Pacific and away from the West (Quah, 2011; UNCTAD, 2021).

Strong momentum towards Asia even before the agreement …

Obviously, the dynamics whereby RCEP impacts the future of trade will mostly depend on China, RCEP’s dominant trade member. China alone takes up over half of the RCEP population and production. In addition, its role in international trade grew exponentially after its entry into World Trade Organization in 2001. Twenty years after its entry into WTO, EU trade with the RCEP members increased significantly: imports as a share of the total increased by 4.5p.p and export by 3.1p.p (see Figure 1, left). This trade boom with RCEP mostly attributes to China and at the expense of some other members like Japan whose export to the EU (as a share of the total) decreased from 2.8% to 1.2% over the corresponding period. The same narrative applies to Austria (Figures 1, right), although the RCEP 2020-2001 increase in trade share is smaller than for the EU as a whole.

… especially for high-tech products

However, the share of EU total imports from RCEP increased much more for high-tech goods (see Figure 2): from roughly 15% in 2001 to 24% in 2020. For Austria, the increase is even higher – a jump of 14p.p in the 20-year-period (Figure 2, right). Nowadays, almost 43% of total EU imports of computer, electronic and optical products, 26% of computer, electronic and optical products, and about 20% of machinery and equipment are sourced from the RCEP bloc. The export with the RCEP members also increased, although it represents lower shares of total EU and Austrian exports (see Figure 3).

This makes this sector particularly dependent and thus vulnerable given the further shift toward Asia and the potential changes in trade patterns resulting from the RCEP agreement. With this comes greater economic implications too, as the high-tech sector relies much more on R&D and innovation than traditional manufacturing. As such, high-tech sectors are an important catalyst of technological growth (Hornbeck and Moretti, 2018), especially in the times of digital and green transition. The obvious sign of risks already exists in relation to the recent semiconductor shortage, which put the production of many EU factories at a halt.

However, stagnation of trade relations in the last year

Even though only one year after the agreement implementation elapsed, we can witness a smaller decline or a stagnation of EU-RCEP trade (see Figure 1 and 2). EU export to the RCEP declined by about 1p.p, while Austrian high-tech imports from RCEP decreased by about 3p.p, the largest decline in high-tech trade with the new trade block in last 20 years. Not surprisingly, this shift is mostly driven by China alone (annual decline of 3.5p.p). This annual decline could be only a tip of the iceberg.

It is difficult to distinguish what drives this decline in the EU-RCEP trade as there are many factors at play. After the COVID-19 pandemic, new trends are on the trade horizon (i.e. nearshoring, reshoring, friend shoring) all marking the start of shorter supply chains, away from globalization. In line with this is RCEP trade bloc that is expected to contribute to the formation of the supply chain across the Asian-Pacific. On the other hand, the ‘EU’s Open Strategic Autonomy by 2040’ assumes a higher economic relationship between the EU and its neighborhood as well as its further trade positioning with respect to China. Besides this, the European Chip Act enacted in December 2022 aims to strengthen the resilience of the high-tech supply chains – precisely the EU semiconductor products for which the demand will double by 2030 according to the European Commission. All these trends should strengthen trade between geographically close countries at the expense of more distant countries. Hence, it is very reasonable to speculate that the next twenty years may bring lower trade with the RCEP due to trade distortion effects (see e.g. Stehrer and Vujanovic, 2022) resulting from the agreement, as well as further trade decoupling.

References

Hornbeck, R., & Moretti, E. (2018). Who benefits from productivity growth? Direct and indirect effects of local TFP growth on wages, rents, and inequality (No. w24661). National Bureau of Economic Research.

Quah, D. (2011). The global economy’s shifting centre of gravity. Global Policy, 2(1), 3-9.

Stehrer, R., & Vujanovic, N. (2022). The Regional Comprehensive Economic Partnership (RCEP) agreement: Economic implications for the EU27 and Austria (No. 054). FIW.

UNCTAD (2021), A new centre of gravity: The Regional Comprehensive Economic Partnership and its trade effects.

Nina Vujanović is an economist at wiiw, researching topics on international trade, foreign direct investment, and the Balkans. She previously worked as an advisor to the Vice Governor at the Central bank of Montenegro, as a consultant at UNCTAD (Division on Investment and Enterprise) and a research fellow at the WTO (Economic Research and Statistic Division). She published papers in the area of foreign direct investment, productivity, innovation as well as credit risk. She holds a PhD in International Economics from Staffordshire University and Msc in Economic Policy from University College London.

The interactive graphics were created by Alireza Sabouniha. He is a research assistant at wiiw and a master’s student in Economics at the WU (Vienna University of Economics and Business).

In her State of the European Union address this year, EU-Commission President Ursula von der Leyen stressed the need to rethink the European Union’s foreign policy agenda and to intensify cooperation with democratic nations (“the core group of our like-minded partners: our friends in every single democratic nation on this globe”) (Von der Leyen, 2022). Latin America plays an important role here. Thus, in the near future, the agreements with Chile, Mexico, in addition to the one with New Zealand, are to be ratified and the negotiations with Australia and India are to be advanced (ibid.). In concrete terms, this means modernising the trade part of the EU-Chile Association Agreement, ratifying the EU-Mexico Association Agreement and the free trade agreement with New Zealand. Furthermore, a comprehensive engagement strategy is to be pursued in Latin America, in cooperation with the G7, especially the USA (ibid.). Latin America thus fulfils two geopolitically important criteria for the European Commission: almost all states are democratically governed, and it is rich in raw materials, also illustrated by the action plan on the EU’s resilience to critical raw materials.

This article focuses on the economic importance of EU trade with Latin America. In total, the EU exported goods worth almost 2.2 trillion Euro to third countries in 2021. Of these, goods worth 114.9 billion Euro were exported to Latin America. This contrasted with imports from Latin America worth 98 billion Euro, resulting in a trade surplus with Latin America of 16.9 billion Euro from the EU’s perspective. As Figure 1 shows, the EU trade balance with Latin America has always been positive in the years since the global financial crisis (from 2012).

In relation to EU exports, Latin America thus plays a comparatively minor role with a share of 5.3% of total in 2021 (Figure 2). By far the most important destination region for EU exports were European third countries, which accounted for 34.5%, followed by Canada and the USA with 20%, China with 10.3% and Africa with 6.7% of the total. Other important export partners by volume are Japan with 2.9%, Korea with 2.4% and India with 1.9% of the total export volume to third countries.

Compared to 2011, the share of EU exports to Latin America in total EU exports actually fell slightly from 5.7% to 5.3%. While the volume of trade with Latin America has grown by around 23.9% since 2011, total EU exports increased by 34.3% (Figure 3). By comparison, exports to China and Canada and the US grew particularly strongly, each increasing by around 77% over the same period.

Within Latin America, the European Commission’s prioritisation reflects the relevance of Chile and Mexico for European export markets. Mexico is the European Union’s most important trading partner in Latin America, followed by Brazil (included here in Mercosur) and Chile (Figure 4).

The negotiations on the EU-Mercosur Association Agreement have been concluded, but the agreement itself is currently “on ice”. From the EU’s point of view, the main obstacle to the ratification of the Association Agreement have been reservations about environmental protection. In Brazil, which dominates the Mercosur group, environmental protection has been weakened on many levels under the Bolsonaro government, and deforestation and the further development of the Amazon region have been promoted. In concrete figures, this means that in 2021 alone, more than 13,000 km² of rainforest (which is more than the area of Tyrol) was cleared, and in 2022 even more. The agreement would take such environmental reservations into account, but as Grübler at al. (2020) conclude, that a trade agreement cannot be a better instrument for enforcing environmental commitments than an environmental treaty. Whereby such clauses are not new in themselves. Environmental clauses in free trade agreements in general have increased significantly since the 1990s (Meinhart, 2022).

With Brazilian President-elect Luiz Inácio da Silva, a new window of opportunity to ratify the agreement could open up. During his election campaign, he announced his goal of concluding the agreement within six months of his re-election, but also him wanting to renegotiate parts of the agreement. At the COP27 summit, as well as previously, he emphasised that combating deforestation in the Amazons will have the highest priority. His credibility in this respect is demonstrated by the significant reduction in deforestation under his presidency from 2003 to 2010. With a view to the European Parliament elections in 2024, where a deal seems unlikely during the election campaign, a window of opportunity opens up for both sides in 2023. The EU’s foreign trade policy is certainly facing a conflict of goals between geopolitical and trade policy interests and the goals it has set itself for the Green Deal. Latin America is a good example of this, with the great economic importance of agricultural and raw material exports on the one hand and the EU’s need for raw materials on the other. Almost 41% of Latin American exports are currently accounted for by raw materials such as rare earths and agricultural goods, and a further 17.8% (as part of the production of material goods) by the production of food and animal feed (Figure 5). In contrast, more than 95% of European exports to Latin America are material goods. The most important sectors from the EU’s point of view are machinery and vehicles as well as chemical and pharmaceutical products.

Latin America is thus relevant for the supply of critical raw materials to the European Union. For example, the European Commission expects EU demand for rare earths, currently dominated by China, to increase fivefold by 2030, and even eighteenfold for lithium. According to the EU Action Plan for Critical Raw Materials Resilience published in 2020, the European Union sources rare earths almost exclusively (98%) from China (European Commission, 2020). In contrast, for lithium, which is particularly important for battery production, Chile is the world’s largest producer and the most important supplier for the European Union (ibid.) Mexico, for example, is the largest non-Asian processor of bismuth and Brazil, likewise among the main producers of several critical raw materials. In the race with China, Latin America accordingly already plays an important role, whose relevance for the EU – especially also in the context of the current geopolitical changes – will increase.

References:

European Commission. (2020). Communication of the European Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Critical Raw Materials Resilience: Charting a Path towards greater Security and Sustainability COM(2020) 474 final, Brussel.

Grübler, J., Reiter, O. und Sinabell, F. (2020). EU und Mercosur – Auswirkungen eines Abbaus von Handelsschranken und Aspekte der Nachhaltigkeit. WIFO Monatsberichte 11/2020.

Meinhart, B. (2022). Greening Trade? Environmental Provisions in Trade Agreements. FIW- Policy Brief, (55).

Von der Leyen, U. (2022). Lage der Union. Rede. https://ec.europa.eu/commission/presscorner/api/files/document/print/de/speech_22_5493/SPEECH_22_5493_DE.pdf

Bernhard Moshammer is Economist at wiiw. His research focuses on European economic and political-economic issues. He has previously worked for the Austrian Federal Chancellery on EU affairs and on housing policies at the Austrian Chamber of Labour. He holds a degree in Economics from the Vienna University of Economics and Business and an M.A. in European Interdisciplinary Studies from the College of Europe, Natolin Campus in Warsaw, Poland.

Since the start of 2022 the euro depreciated by some 15%, beginning the year at 1.14 USD per EUR and declining below parity towards 0.97 recently. One major factor causing this decline can be viewed as truly exogenous: the war in Ukraine was unexpected and resulted in several rounds of sanctions imposed on Russia, with sizeable negative repercussions on the EU’s export volumes and impairments for active foreign direct investment (FDI) of EU-firms in Russia. The EU received a second blow through rising energy prices. Many member countries showed a high dependence on Russian gas and oil, and the Russian government deliberately used its position to generate uncertainty in spot as well as futures gas markets leading to severe risk premiums after sanctions and countervailing measures by Russia were going back and forth. Due to its high dependence on Russian energy, the euro area suffered a set-back as a business location, making the euro area less attractive for passive FDI, destroying potential output, and finally leading to a depreciation of the euro vis-a-vis areas less exposed to Russia as a trade partner.

There is a second endogenous source for the devaluation of the euro, resulting from the build-up of inflationary pressure throughout the world economy, except Japan. The US-Federal Reserve Bank (Fed) was first confronted with rising inflation rates since in April 2021 (+4.2% YoY) while inflation in the euro area at that time still remained below target (+1.6% YoY). Both monetary authorities interpreted higher inflation rates as energy driven and transitory but by December 2021 the Fed changed its opinion and corrected its forward guidance from accommodative to restrictive. The Fed first announced to unwind its asset purchase program and started to increase the target rate by March 2022, while the ECB waited until the end of July 2022 to follow suit. By the end of September 2022 the target range for the US-interest rate reached 3% to 3.25% and the euro area‘s main refinancing rate was at 1.25%, creating an interest rate differential of almost 2 percentage points.

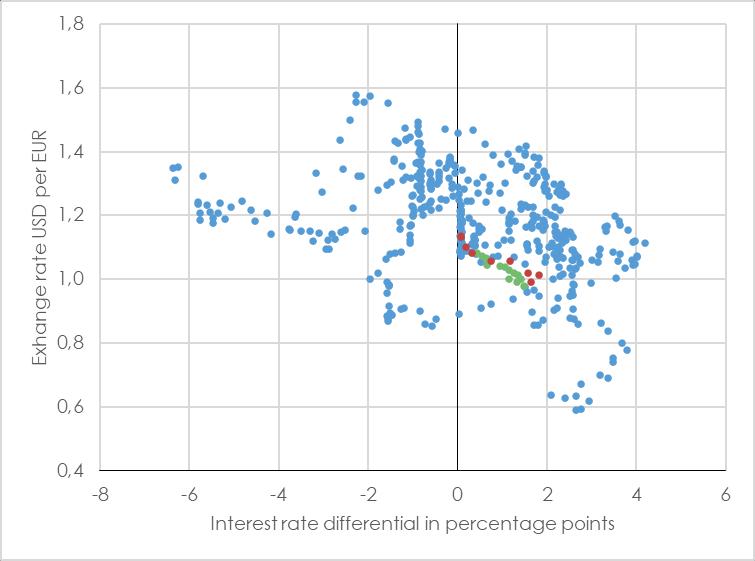

Deviations between US and European short term interest rates were a regular feature in the past. Figure 1 shows the interest rate differential between the US-target rate and the corresponding European equivalent from 1985 through 2022. A positive value on the horizontal axis implies that US-rates were above the main refinancing rate in the euro area. The vertical axis shows the exchange rate measured in USD per EUR. The slight negative slope of this cloud indicates that relatively high target rates in the US go along with a strong US-dollar, while a relatively high refinancing rate in the euro area typically involves a strong euro. The red dots in Figure 1 show the development from January to September 2022; the movement towards the lower right hand corner reflects the more aggressive policy stance in the USA together with the appreciation of the US-dollar.

Figure 1 – Relatively higher domestic interest rates support the home currency

Starting from this situation, what can we expect for the rest of 2022 and the following year? The WIFO forecast (Glocker – Ederer, 2022) expects a further tightening of monetary policy in both areas with the ECB acting more decisively such that the interest rate differential will be reduced to around 0.5 percentage points at the end of 2023. Accordingly, the euro will appreciate slightly (green dots in Figure 1), resulting in annual averages of 1.05 (2022) and 1.04 (2023) USD per euro with a trough in fall 2022. This development can be interpreted using the uncovered interest rate parity condition: after the US-monetary tightening, the USD must jump to a lower value (appreciation) in order to keep the interest parity condition valid, thus providing room for a consecutive depreciation which balances higher US-interest rates (Dornbusch, 1976). This adjustment mechanism does not hold empirically, however (Engel, 2014). A time-variable degree of asset market segmentation (Alvarez et al., 2009) or a liquidity premium on the deposit earning higher interest (Engel, 2016) provide alternative explanations.

Does the USD-EUR exchange rate actually jump around announcements dates of monetary policy actions? Figure 2 offers some insight. The lines in Figure 2 depict the exchange rate during the 10 business days before and after a monetary policy meeting, on which either the Fed (green) or the ECB (blue) announced a change in their target rate. To facilitate comparison, I norm the exchange rate for all episodes to unity at the day of the monetary policy announcement, thus a value of 1.02 indicates that the exchange rate was 2% above the level prevailing at the announcement date. The period runs from 16.3.2022, when the Fed published the first rate-hike through 21.9.2022, when the Fed increased the target range to 3% to 3.25%. Because both central banks explicitly use forward guidance, their moves appear to be somewhat expected. While the ECB does not seem able to move markets, the Fed announcements effectively make the dollar stronger, either at the date of the publication or even five to ten days ahead. Whether the ECB policy decision on 27.10.2022 includes some surprise element for the participants on the foreign exchange market, can be tracked in real time in Figure 2 over the next ten business days following the announcement date.

Finally, will there be consequences from the euro’s depreciation on the real economy? Probably price effects will dominate over the forecast horizon. A weaker euro implies higher import prices on intermediates, energy, consumer products, and tourism services in a period already plagued by inflationary strain. Such an environment makes it easier to pass-through higher import prices on to euro area customers. Positive wealth effects related to foreign USD-denominated portfolio investments by Europeans, however, will not compensate the price losses on international asset markets during 2022. Consequently, the potential positive effect on euro area consumption will remain limited. A cheaper euro will boost euro area exports, but at the same time weak foreign demand is likely to be the dominating force affecting international trade flows.

is Senior Economist at WIFO and has been working in the Research Group “Macroeconomics and European Economic Policy” since 1994. From 1999 to 2002 he was editor-in-chief of WIFO-Monatsberichte (WIFO Monthly Reports). He is an expert in the Austrian Fiscal Council, lecturer at the University of Vienna and head of the Working Group on Economic Statistics and National Accounts of the Austrian Statistical Society. He works on issues of risk diversification, funded pensions, the European Monetary Union and econometric applications in the field of macroeconomics.

The international economic environment has deteriorated significantly since the beginning of 2022, mainly due to the knock-on effects of the Russia-Ukraine conflict, and the outlook for the global economy and global trade has clouded considerably. The energy price shock and the massive price hike, as well as uncertainty about the availability of gas, are causing dislocations above all in material goods production and exacerbating supply-side shortages due to supply bottlenecks and the aftermath of the COVID 19 pandemic. Consumer confidence and corporate production expectations are falling worldwide, most sharply in the euro zone.

Domestic manufacturing and, in particular, exports proved to be very robust in the first half of 2022 in the face of the negative influences of massive increases in raw material and energy prices, labor shortages, supply bottlenecks and high uncertainty. Austrian merchandise exports expanded strongly in the first half of 2022, with extremely dynamic growth in Q1 2022, which – despite the onset of the Russia-Ukraine crisis in March 2022 – continued only slightly weaker in Q2 2022. The growth of exports of goods reached 19.2% at current prices (nominal) and 14.1% at constant prices (real) by June 2022. The widening gap between the nominal and real trends reflects rising export prices. Austria’s goods export performance was hardly outperformed by any other EU country. Germany, France and Italy recorded significantly lower growth, but goods exports of many smaller European comparator countries, such as Sweden, Finland or the Netherlands, also grew more slowly than in Austria.

Industrial intermediate goods (“processed goods”) have so far made one of the highest contributions to growth in total merchandise exports. This was a consequence of still stable industrial production through increased production in stock with key trading partner countries in order to escape threatened shortfalls in energy supplies and further price increases. The equally high contribution to growth made by Austrian machinery exports was due in particular to strong demand from the USA. The high order backlog in the German capital goods industry also contributed to growth in Austria’s machinery exports. The contribution from energy and raw material exports was mainly price-driven rather than due to an expansion in export volumes. The otherwise important Austrian automotive and automotive supply industry made hardly any contribution to export growth. This is closely related to the crisis in the German automotive industry.

Leading indicators, which remained at a high level until the end of Q2 2022, now also point to a sharp slowdown in export momentum in Austria in the second half of 2022. In the WIFO Business Survey, exporters continue to assess order books from abroad as predominantly positive, but the share of positive reports has declined significantly since June 2022. Export expectations have been significantly scaled back for the first time since the COVID-19 crisis, and negative expectations for export business predominate. As a result, the outlook for new export orders for the remainder of the year is much more subdued. In Q3 2022, export growth should still be fed by the high order backlogs of previous months and diminishing material bottlenecks in domestic production. In the further course of the year, the negative consequences of the Russia-Ukraine crisis are likely to have an increasing impact on Austrian exports of goods. Austria’s strong ties with the CEECs and Germany, which are particularly affected by the current crisis, will contribute to this, as will the expected decline in production in Austria’s manufacturing sector due to high energy prices – especially natural gas prices. This effect is amplified by the loss of international competitiveness, especially in non-European exports – currently, European and Austrian industry faces gas prices about seven times higher than those in the U.S., for example, and competitive advantages for exporters due to the devaluation of the euro hardly outweigh this. However, the direct negative effect of energy prices on manufacturing in Austria is likely to be somewhat weaker than in Germany, especially since the natural gas intensity of Austrian industry is somewhat lower.

The forecast assumes that there will be no official business closures due to the COVID 19 pandemic in Austria or in key trading partners that would affect the export industry until 2023. It is also assumed that the Russia-Ukraine war will continue and that the sanctions against Russia will remain in place. It is not assumed that Russia will completely halt natural gas supplies to Europe, but uncertainties, especially regarding price developments, are assumed to remain and thus the level of natural gas prices will remain high. In this environment, some of Austria’s main trading partners are facing a sharp economic slowdown, which will lead to recession in 2023 in Germany, Italy and CEEC. The revisions in the international economic outlook since the beginning of the year have been enormous, shaping the forecast picture of all major international organizations (European Commission, OECD, IMF, World Bank) and reflecting the increasing distortions of the Russia-Ukraine conflict and the strikingly higher world market prices of energy and raw materials. As a result of the cooling of the global economy in 2023, the problem of bottlenecks in supply chains should subside. The situation is also expected to ease for freight rates in international transport and for the prices of crude oil and industrial raw materials.

Under these changed conditions, Austrian export momentum will decline sharply, especially at the end of 2022, but supported by the extraordinarily good performance in the first half of 2022, will lead to annual growth in goods exports of around 8%, almost matching the previous year’s growth (2021: +9.3%). At 10.0%, import prices will rise much faster than Austrian export prices (+5.9%) in 2022. The high world market prices for raw materials, energy and intermediate goods thus cause a strongly negative terms-of-trade shock, which is further amplified by the depreciation of the euro. As a result, the Austrian trade balance will be burdened this year with a negative price effect of around € 8 billion. Positive volume effects due to a smaller increase in import volumes than in export volumes will dampen this negative effect, so that the trade balance is expected to deteriorate by a total of €4.3 billion in 2022 to a deficit of approx. 17 billion in 2022.

Im Jahr 2023 erreicht das österreichische Marktwachstum auf Basis der schwachen internationalen Importprognosen für die